Inclusiv/Mortgage is committed to increasing personal wealth for under-resourced communities through homeownership. We do this by offering our member credit unions a secondary market outlet which offers expanded approval guidelines that make it possible for under-resourced people to qualify for a mortgage. Credit unions have long played an important role in homeownership financing and counseling as part of their historic commitment to serving people of modest means. Inclusiv’s homeownership initiatives aim to increase community development credit unions’ recognition as a source of responsible mortgage financing and to expand credit unions’ capacity as mortgage lenders and providers of accurate and consistent homeownership counseling.

Inclusiv/Mortgage

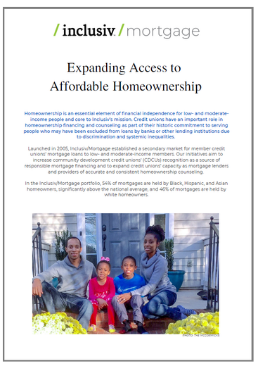

Launched in 2005, Inclusiv/Mortgage established a secondary market for member credit unions’ mortgage loans to low- and moderate-income members. As of January 2022, Inclusiv's mortgage portfolio is comprised of $20 million in affordable home mortgages originated by 30 community development credit unions across the country.

Launched in 2005, Inclusiv/Mortgage established a secondary market for member credit unions’ mortgage loans to low- and moderate-income members. As of January 2022, Inclusiv's mortgage portfolio is comprised of $20 million in affordable home mortgages originated by 30 community development credit unions across the country.

Inclusiv/Mortgage is a Secondary Market Program that purchases conforming and non-conforming affordable first lien mortgage loans from our member credit unions who are approved to sell loans to Inclusiv. By creating a pipeline for CDCUs to sell their mortgages, Inclusiv/Mortgage replenishes credit unions’ capital, reduces rate risk & enabling CDCUs to magnify their impact in their communities. Inclusiv/Mortgage helps CDCUs recycle capital in their communities, freeing up funds for additional lending. In 2016, Inclusiv/Mortgage launched a new initiative to dramatically increase the volume of loans purchased, providing an alternative to the predatory practices targeted at the minority, immigrant and low-income communities across the country, enabling our member credit unions to provide quality residential mortgage services to the communities they serve.

The FLOW Program

Under this program, the credit union originates, processes, underwrites, and closes loans to Inclusiv/Mortgage guidelines. After closing, the credit union sends the loan to Inclusiv/Mortgage for purchase. This process usually takes less than one week.

Under the Flow Program, there are two loans:

- INCLUSIV 97 - A 30-yr fixed rate loan & a 5/1 & 10/1 adjustable-rate mortgage for borrowers with a social security number. LTVs are up to 97% with very low PMI rates that max at 18%

- INCLUSIV ITIN – A 10/1 & a 5/1 adjustable-rate mortgage up to 90% LTV for borrowers with an ITIN number. Please note that LTVs over 80% are subject to minimum loan amounts.

Both loans have minimum credit scores of 580 and the maximum DTI is 45%. Borrowers without traditional established credit can be qualified using alternative credit sources, and borrowers with multiple sources of income are qualified the same as self-employed borrowers

The BULK Program

Under this program, Inclusiv/Mortgage will buy blocks of seasoned loans from credit unions looking to free up capital and/or reduce rate risk. Loans must be seasoned at least 12 months. Loans under 12 months can be purchased with temporary recourse that ends when the loans reach 12 months of seasoning. The minimum credit score is 550, maximum DTI is 50%, and maximum LTV is 97%.

Rates

Inclusiv/Mortgage offers more competitive rates for lower credit scores and higher LTVs, and pays higher premiums for these loans. This change was made to make a bigger impact with low to middle income borrowers. Additionally, rates for the adjustable rate mortgages for ITIN borrowers are the same as for borrowers with a social security number.

Servicing Option

Credit unions who prefer to retain servicing may do so if approved by Inclusiv/Mortgage. This application process is streamlined for credit unions who are already approved to service for Fannie, Freddie, or FHLB. For credit unions who can not or do not want to retain servicing, our master servicer CUMA (Credit Union Mortgage Association) will service all purchased loans.

Outsourced Processing & Underwriting

For credit unions who prefer not to process and underwrite loans in-house, we have partnered with CUMA to perform this function for you. CUMA will process and underwrite to Inclusiv/Mortgage guidelines so you can close and sell your loans to Inclusiv with peace of mind. This service can be applied to all your loans, not just the loans you want to sell to Inclusiv.

Down Payment Assistance Grants

Inclusiv/Mortgage is now offering Down Payment Assistance (DPA) grants for first-time homebuyers who meet program guidelines. Each grant is up to 1.5% of the purchase price, not to exceed $2,500 and must be attached to loans sold to Inclusiv/Mortgage. Minimum first mortgage LTV is 90% for Inclusiv 97 and 90% for Inclusiv ITIN loans. Borrowers must be at or below 80% of the area medium income. All grants have 5-year forgivable terms, and payback will only be required if the property is sold or refinanced prior to the 5-year term ending and will be prorated based on 60 months with no interest. There is a limit of 3 grants per credit union until further notice.

Get the DPA term sheet.

2nd Look Program

All lenders have a percentage of loans that are declined every month, usually through automation, but many do not have a plan in place to review those declinations. At a recent webinar we held last year, 40% of the audience had no plan whatsoever in place. To try to save some of those loans, Inclusiv/Mortgage instituted a 2nd Look Program. Inclusiv approved sellers can take their declinations, fill out one of our Declination Quick Look Sheets and submit to Inclusiv/Mortgage for review. Since its inception in September of 2021, the program has proven to be a huge success. Of all the declinations submitted, as of February 2022 we are operating at a 57% success rate turning these declinations into approvals. This is enabling us to expand the scope of our impact to under-resourced communities and is a huge win for everyone involved.

What’s coming up in 2023?

- Our Puerto Rico Pilot program was officially launched at our conference in May of 2022. We are still working out the legal details so stay tuned for updates later in 2023.

- Inclusiv/Mortgage is planning on adding participations to our offerings. We are currently working out the details and are excited to be able to start offering these to interested credit unions. Participations are a great way to help bolster loan portfolios, increase income streams and help credit unions to hit their CDFI targets, which in turn helps them to qualify for CDFI grants. Look out for this later in the year.

How to Apply

Inclusiv/Mortgage accepts applications from member credit unions interested in selling qualifying mortgages on an ongoing basis. This process is streamlined for credit unions already approved by Fannie, Freddie or FHLB.

For more information or an application to sell, please contact Inclusiv/Mortgage at mortgage@inclusiv.org.