We are excited to share this update on Consumer Finance for Climate Action (CFCA), a collaborative effort led by Inclusiv and SaverLife to identify and develop practical products, services, and policies that support low- and moderate- income households in the face of climate change.

Share

Building Financial Resilience in The Face of Climate Change

September 19, 2024

How CFCA is Activating Innovative Solutions to Support Climate Resilience and The Financial Well-being of Households with Low-to-Moderate Incomes

Why CFCA

Climate change is increasingly affecting the everyday lives of households across the United States. Weather events, from storms to flooding to fires, have become both more common and more severe. Chronic conditions, such as excessive heat and poor air quality have also increasingly become a regular part of life for families in every state and region across the U.S.

While all U.S. households increasingly feel the effects of climate change, the impacts disproportionately affect low- and moderate-income (LMI) households, who are both more likely to be negatively impacted (based on their lack of financial security, where they live, what jobs they have, the condition of their housing, etc.) and have fewer resources to prepare for and respond to climate change. The negative effects of climate include both catastrophic events, like property damage or loss of a home, and more everyday impacts, like power outages or rising utility costs. In addition to increasing the financial resilience of LMI households, we need all households to benefit from climate solutions, whether that means switching to more energy efficient appliances, installing rooftop solar, or driving an electric vehicle.

Inclusiv and SaverLife are working together to create CFCA in response to this duality: that low-income households need to benefit from climate solutions and increase their financial resilience in the face of climate change – and yet, they have less ability to do either.

What CFCA Will Do

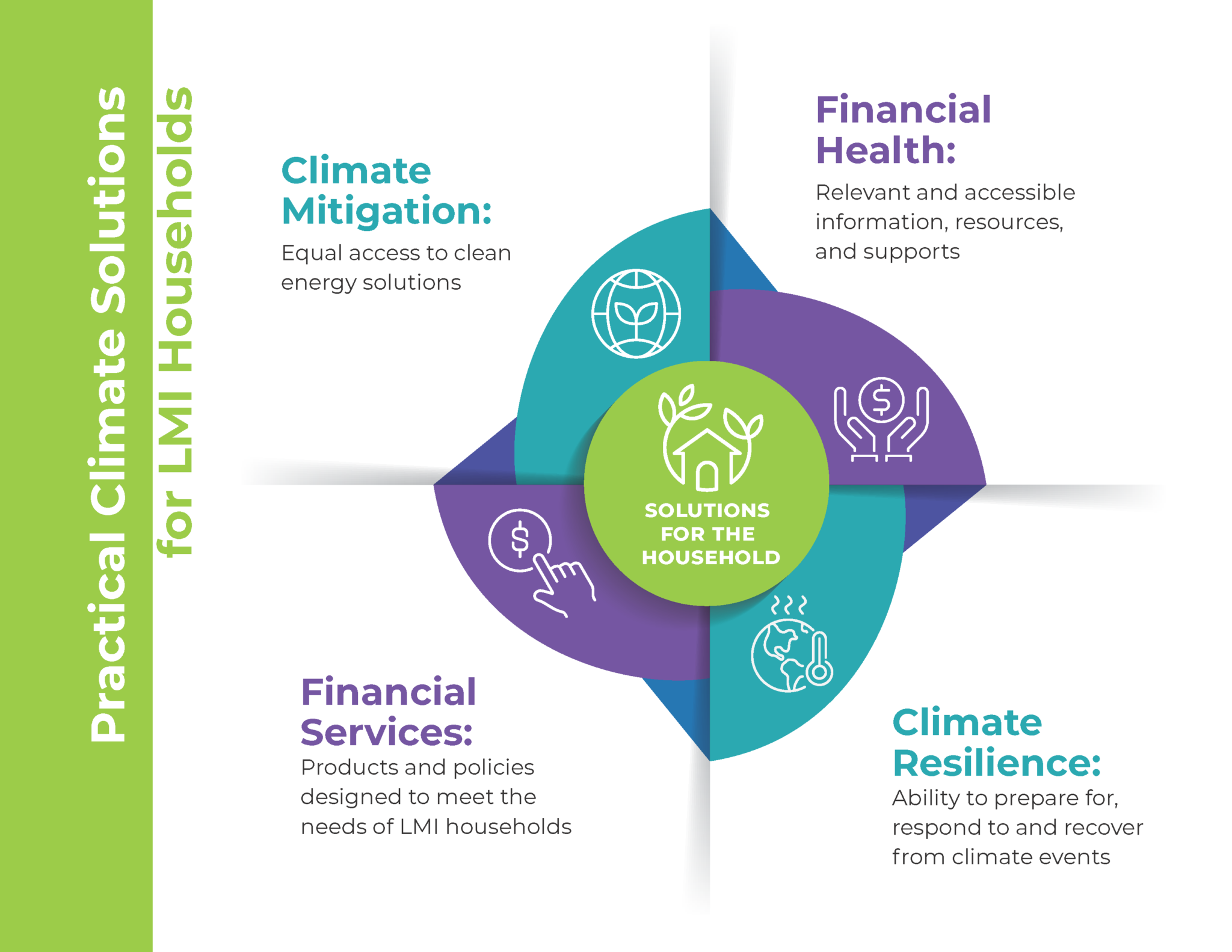

The goal of CFCA is to identify and lift up innovative solutions that address climate change and support the financial well-being of households with low-to-moderate incomes. Those solutions fall under the umbrellas of both financial services and financial health, and these two fields will need to work closely together to provide families with the supports they need to weather this crisis.

Getting CFCA off the Ground

SaverLife and Inclusiv launched this effort at the 2024 Inclusiv Conference in New York, which included a Conference plenary, track of workshops, and roundtable working session with stakeholders from multiple sectors, including:

- Climate equity and advocacy

- Credit unions and green lending

- Disaster relief

- Financial health

- Green energy transition

- Housing and community development

- Philanthropy

- Other related sectors

The workshops and roundtable reaffirmed a commitment to center LMI households in climate resiliency and decarbonization solutions. It provided an initial step in prioritizing problems faced by households and honing effective solutions. As LMI households are increasingly impacted by climate events, there is an urgency to support solutions that will boost resiliency, affordability, and financial security.

In June, SaverLife released a second report in its Downpour series: Closing the Gap: Building Climate Resilience by Meeting the Demand for Clean Energy Solutions. That report builds on the learning from the initial Downpour research, which found that climate change is already impacting the finances of LMI households, that those households are struggling to prepare for and respond to climate events, and that they are interested in implementing green solutions but face barriers in doing so. The new report focuses on opportunities created by the Inflation Reduction Act (IRA) – as well as risks that it’s provisions could further increase the divide between families that are financially able to engage in climate solutions and those that are not.

For example, SaverLife’s research found that only 6% of those surveyed say they have solar panels, but 46% are interested in them. The gap was even greater for energy efficiency solutions that can reduce costs and improve quality of life, such as home weatherization or energy efficient appliances. And yet, many of the incentives and subsidies available to families take the form of rebates and non-refundable tax credits, which can be complicated to access, and which may not be available to low-income tax filers or renters.

The work of CFCA – practical climate solutions targeted to the needs of LMI households – is more critical than ever. Solutions for LMI families may take many different forms, including increased subsidies, affordable loans, emergency cash, help accessing available programs, help choosing a reputable provider or contractor, or of advice on what action or upgrade will provide the greatest impact on a family’s monthly budget. As we build out CFCA, we will look to both help consumers navigate the existing marketplace and fill gaps in that marketplace.

What's Next for CFCA

To ground CFCA in a coordinated understanding across climate action, community development finance and financial health, CFCA commissioned a landscape analysis (with input from nearly 40 stakeholders across multiple fields). Over the coming months, Inclusiv and SaverLife will publish and disseminate the landscape analysis and lead cross-sector convenings to structure a comprehensive approach to support LMI households in both climate mitigation and climate resiliency.

CFCA also plans to expand the reach of SaverLife’s Downpour research through Inclusiv’s network of Community Development Credit Unions. Ultimately, these activities will inform the future development of a CFCA business plan, focused on practical solutions that financial institutions and financial health providers can implement to support LMI households in the face of climate change.